Purchasing a new car is an exciting experience, and ensuring it’s properly protected is a crucial step in the process. For the most part, insuring a new car doesn’t fundamentally differ from insuring any other vehicle. The type and amount of car insurance coverage you need are primarily determined by factors like your location and any specific requirements from your lender if you’re financing your new car with a loan.

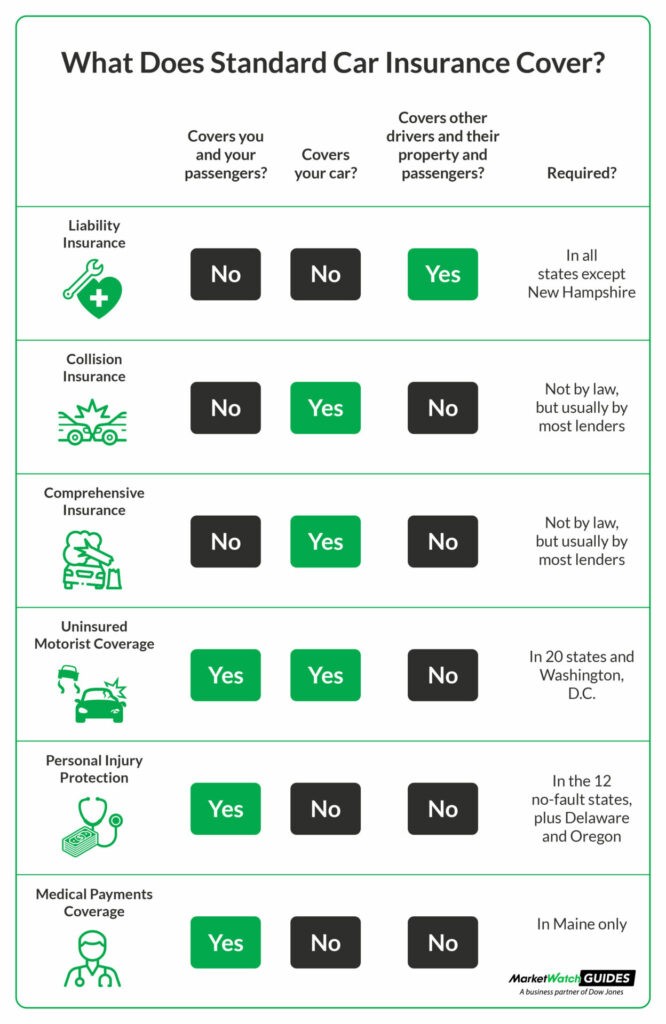

Chart detailing six standard types of car insurance coverage, including liability, collision, comprehensive, uninsured/underinsured motorist, medical payments, and personal injury protection.

Chart detailing six standard types of car insurance coverage, including liability, collision, comprehensive, uninsured/underinsured motorist, medical payments, and personal injury protection.

Understanding State Minimum Car Insurance for New Vehicles

Each state sets its own minimum car insurance requirements. These regulations, typically established by the state’s Department of Motor Vehicles (DMV) or a similar agency, can vary significantly from state to state. To understand the specific insurance obligations in your location, it’s essential to consult your state’s DMV website or resources from your insurance provider. Knowing these minimums is the first step in ensuring you are legally compliant and adequately protected when you drive your new car off the lot.

Common Types of Required Car Insurance Coverage

State minimum insurance requirements usually consist of variations of the standard auto insurance coverage options. These foundational coverages are designed to protect you and others on the road in case of accidents or damages. Understanding these standard types is key to making informed decisions about your new car insurance policy, going beyond just the minimum requirements to ensure comprehensive protection.

Lender Requirements for New Car Insurance

If you’re taking out a loan to finance your new car, your lender will likely have specific insurance requirements beyond state minimums. These additional stipulations are in place to protect the lender’s financial investment in the vehicle. Lenders want to ensure that the car, which serves as collateral for the loan, is protected against damage, loss, or theft. This is why they often mandate that borrowers carry certain types of coverage that specifically safeguard the vehicle itself, regardless of fault in an accident. Failing to meet these lender-imposed insurance requirements can sometimes lead to the lender force-placing insurance on your vehicle, which is typically more expensive and less comprehensive than a policy you would choose yourself.

Additional Car Insurance Options for New Car Owners

While standard and lender-required coverages focus on basic protection and financial security for loans, there are numerous additional car insurance options that can enhance your peace of mind as a new car owner. These optional coverages address various aspects of car ownership, from unexpected breakdowns to everyday conveniences. Many insurance companies offer a range of these add-ons, allowing you to customize your policy to fit your specific needs and driving habits.

Here are some of the most frequently offered optional coverages:

- Roadside Assistance: This coverage is invaluable for unexpected car troubles. It covers services like towing your new car to a repair shop, delivering fuel if you run out of gas, and repairing or replacing a flat tire. Roadside assistance can save you from being stranded and incurring out-of-pocket expenses for these common emergencies.

- Rental Reimbursement: If your new car is in the shop for repairs due to a covered accident, rental reimbursement coverage helps pay for the cost of a rental car. This ensures you have transportation while your vehicle is being fixed, minimizing disruption to your daily routine.

- Mechanical Breakdown Insurance (MBI): MBI is similar to an extended car warranty but is offered by insurance companies. It covers repairs to certain mechanical components of your new car after a breakdown, protecting you from potentially high repair bills down the line, especially as new cars can still experience mechanical issues.

- Rideshare Insurance: If you plan to use your new car for ridesharing services like Lyft or Uber, rideshare insurance is essential. It bridges the gap in coverage that may exist between your personal auto policy and the coverage provided by the rideshare company, particularly during periods when you are logged into the app but are not actively transporting passengers.

- Travel Expenses Coverage: Should you experience a covered loss while driving your new car away from home, travel expenses coverage can help with costs for food, lodging, and other travel necessities. This coverage provides a safety net if you are stranded away from home due to car trouble.

Most car insurance providers offer a diverse selection of optional coverages tailored to new car owners. To fully understand the available options and what each plan entails, it is always recommended to speak with an insurance agent. They can provide personalized advice and help you choose the right coverage to protect your new car and your financial well-being.